Navigating today’s complex financial landscape demands that tax-sensitive investors remain vigilant against potential traps that could significantly impact their after-tax returns. Staying informed and proactive will help you manage your tax burden more effectively and protect your wealth. In this guide, we outline 5 TAX TRAPS that deserve your attention now.

1. CAPITAL GAIN DISTRIBUTIONS: NAVIGATING THEIR IMPACT IN ANY MARKET ENVIRONMENT

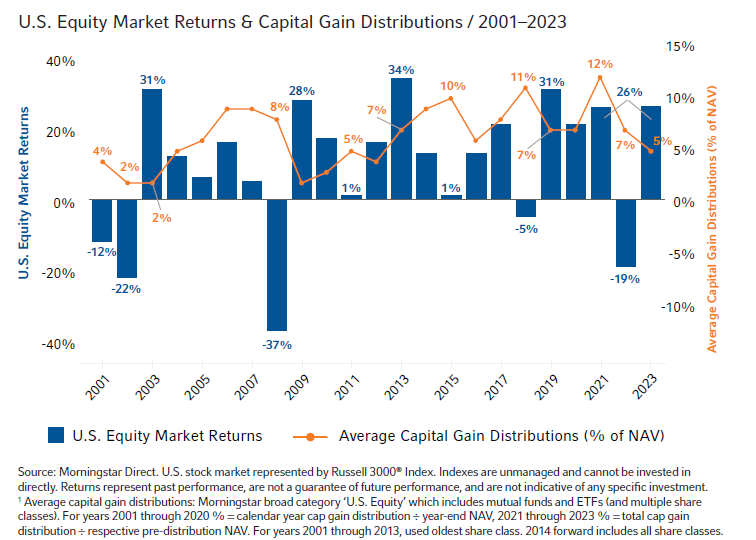

Each year, mutual funds calculate their realized gains and losses for the fiscal year (typically November 1– October 31). If the gains exceed the losses, the net amount is distributed to investors as a capital gain. For taxable investors, it’s important to consider the tax implications of these distributions.

The chart below illustrates the average mutual fund distribution¹ as a percentage of a fund’s Net Asset Value (NAV), compared to U.S. stock market returns since 2001. Notably, the average capital gain distribution has never been 0%. In fact, some of the largest distributions occurred in years with flat or negative market returns (e.g., 2008, 2015, and 2018). Regardless of market performance, the impact of capital gains taxes remain a significant consideration.

Reviewing potential capital gain distributions in your current investments can help you determine if transitioning to tax-managed investing is appropriate for your financial strategy.

2. TAX-LOSS HARVESTING: A YEAR-ROUND OPPORTUNITY

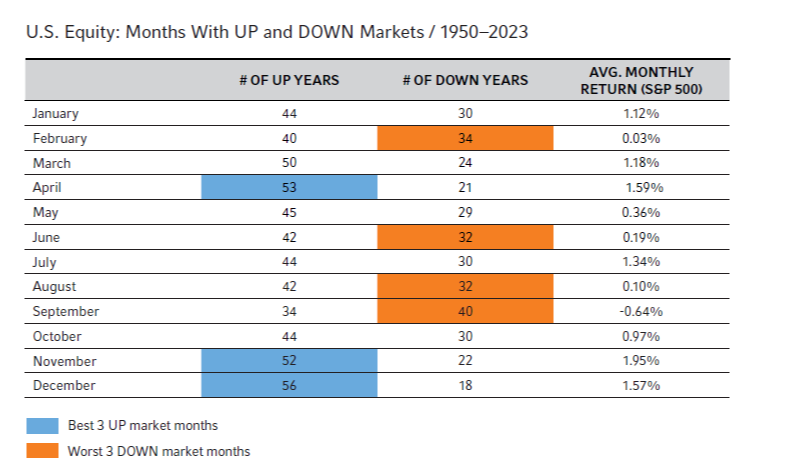

Each year, market pullbacks create opportunities for tax-loss harvesting. While investors often focus on taxloss harvesting at year-end, historical market data spanning 74 years indicate that November and December are among the three best-performing months of all. That makes them less attractive for harvesting losses.

It’s crucial to actively manage taxes throughout the year to help reduce any potential tax burden when market volatility emerges. In addition to tax-loss harvesting, consider other strategies that can be

implemented at various points throughout the year to maximize after-tax returns.

Don’t limit tax management to a basic year-end activity. Explore timely tax strategies throughout the year for potentially better financial outcomes.

3. CASH ON THE SIDELINES: WATCH OUT FOR THE TAX BITE ON INTEREST INCOME

While Certificates of Deposit (CDs) and Money Market Funds may seem compellingly attractive with their high yields, it’s important to examine their real return after inflation and the impact of taxes. CDs are subject to ordinary income tax rates, which can reach as high as 40.8%* when federal income taxes are included. A better after-tax option could be municipal bond funds which offer a tax advantage with a 0% federal tax rate**, allowing you to retain more of your earnings.

Furthermore, you should consider the potential impact of inflation on the purchasing power of your investment returns. It’s essential to look beyond surface-level returns and evaluate the broader financial

picture. This approach ensures you make the most informed and tax-efficient investment decisions.

4. POTENTIAL TAX INCREASES ON THE HORIZON: THE SPECTER OF RISING FEDERAL DEBT

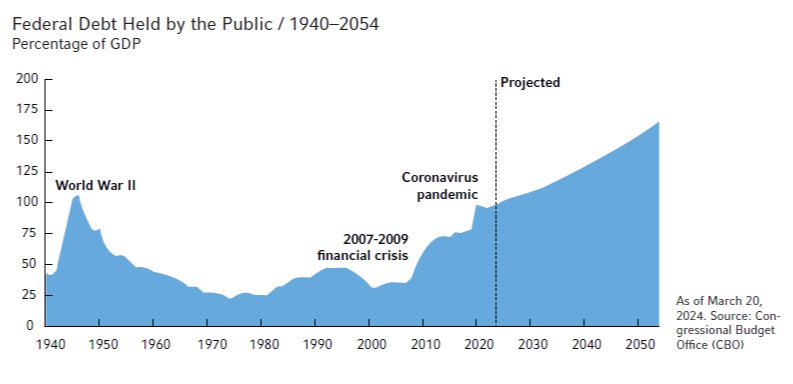

U.S. public debt surpassed $35 trillion in July 2024. By 2029, the government’s debt climbs to 107% of GDP, exceeding the historical peak it reached immediately after World War II. The Congressional Budget Office predicts this debt will continue to increase every year for the next 30 years. In 2054, it reaches 166% of GDP and will likely continue increasing over time. To address this growing debt burden, the government will most likely need to raise taxes in the future.

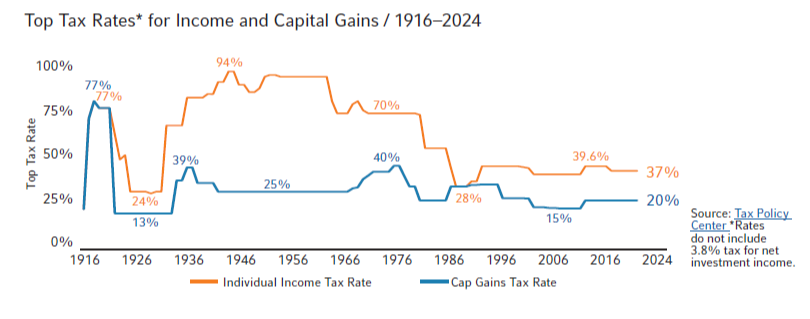

As we look ahead, understanding the historical trends in tax rates is essential. This chart showcases the top income and capital gains tax rates from 1916 to 2024, highlighting significant shifts over time. With potential tax changes on the horizon, it’s important to consider how these shifts could impact investment portfolios, regardless of past perceptions.

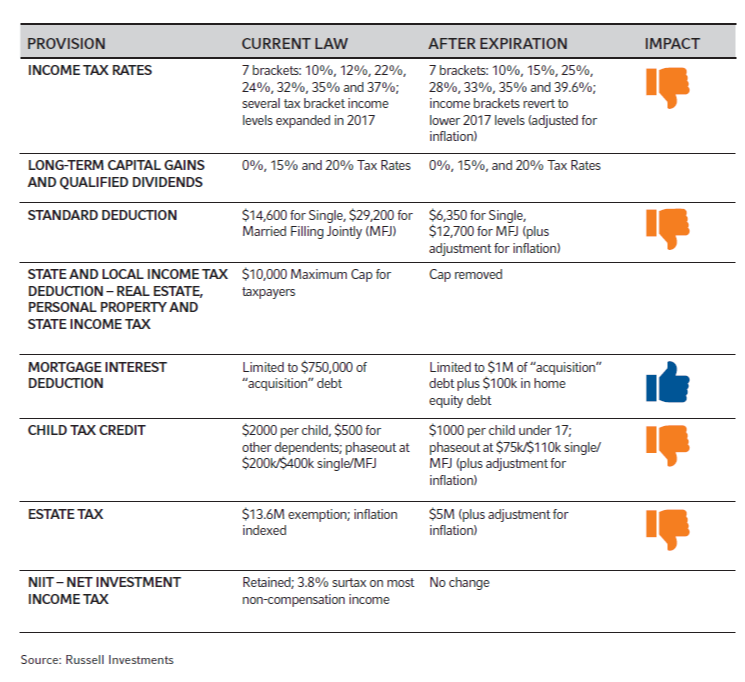

5. TAX CUTS AND JOBS ACT (TCJA): ONLY TWO TAX FILINGS LEFT BEFORE IT SUNSETS

With just two tax filings remaining before the potential sunsetting of the Tax Cuts and Jobs Act (TCJA), it’s crucial for investors to prepare for any changes in tax policy. Most of the TCJA’s individual tax provisions, including the reduction in income tax rates, are set to expire after 2025. Without Congressional intervention, this could result in higher taxes, reducing your after-tax disposable income and increasing the burden on your investment gains and income. Be sure to consider the long-term implications of these potential changes when making your financial decisions.

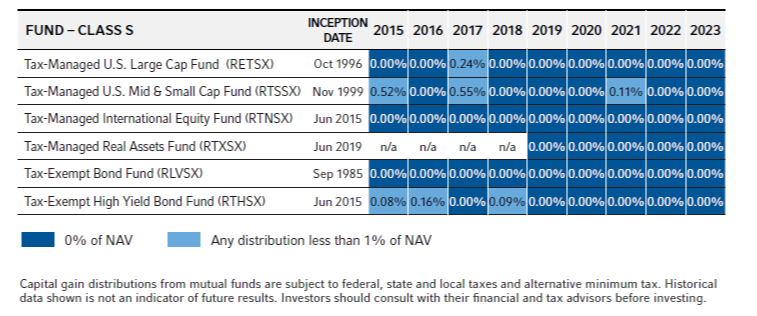

RUSSELL INVESTMENTS: ACTIVE IN THE TAX-AWARE SPACE SINCE 1985

Russell Investments actively manages taxes within each of our tax-managed and tax-exempt funds. Our trading desk is ready 24 hours a day to systematically implement tax-loss harvesting strategies whenever the opportunity presents itself. With a full-year focus on managing taxes, our funds have successfully minimized their tax impact by achieving little to no taxable distributions.

Russell Investment Company Tax-Managed and Tax-Exempt Funds

Annual Capital Gain Distributions (% of NAV)

HOW TO TAKE ACTION TODAY

BEING TAX-SMART IS A YEAR-LONG ENDEAVOR.

Current markets conditions may be challenging for investors, but they also present attractive opportunities to actively manage taxes in a portfolio. Volatility allows for tax-loss harvesting, which creates tax “assets” that can be used to offset future capital gains taxes.

- Here’s how you and your financial advisor can assess your current situation and evaluate whether you may benefit from a tax-managed approach in your investment portfolio.

Create a list of all of your mutual fund investments, the Net Asset Value (NAV) when you purchased them,

and the current NAV. - Calculate the unrealized gains/losses, then sort the list by unrealized gains/losses.

- Review investments that may be suitable for transition, in particular:

- Investments with losses represent an opportunity to create a tax asset in your portfolio to offset

against other gains. - Investments with close to zero unrealized gains/losses.

- Investments with losses represent an opportunity to create a tax asset in your portfolio to offset

IMPORTANT RISK DISCLOSURES

Russell Investments is not affiliated with Community Choice Investment Services or LPL Financial.

Please remember that all investments carry

some level of risk, including the potential loss

of principal invested. They do not typically

grow at an even rate of return and may

experience negative growth. As with any type

of portfolio structuring, attempting to reduce

risk and increase return could, at certain times,

unintentionally reduce returns.

Indices and benchmarks are unmanaged

and cannot be invested in directly. Returns

represent past performance, are not a

guarantee of future performance, and are not

indicative of any specific investment. Index

return information is provided by vendors and

although deemed reliable, is not guaranteed

by Russell Investments or its affiliates. Due to

timing of information, indices may be adjusted

after the publication of this report.

Small capitalization (small cap) investments

generally involve stocks of companies with

a market capitalization based on the Russell

2000® Index. Investments in small cap, micro

cap, and companies with capitalization smaller

than the Russell 2000 Index are subject to the

risks of common stocks, including the risks

of investing in securities of large and medium

capitalization companies. Investments in

smaller capitalization companies may involve

greater risks as, generally, the smaller the

company size, the greater these risks. In

addition, micro capitalization companies and

companies with capitalization smaller than the

Russell 2000 Index may be newly formed with

more limited track records and less publicly

available information.

Investments in global equity may be

significantly affected by political or economic

conditions and regulatory requirements in a

particular country. International markets can

involve risks of currency fluctuation, political

and economic instability, different accounting

standards and foreign taxation. Emerging or

frontier markets involve exposure to economic

structures that are generally less diverse and

mature. The less developed the market, the

riskier the security. Such securities may be less

liquid and more volatile.

Investments in infrastructure-related

companies have greater exposure to the

potential adverse economic, regulatory,

political and other changes affecting such

entities. Investment in infrastructure

related companies are subject to various

risks including governmental regulations,

high interest costs associated with capital

construction programs, costs associated with

compliance and changes in environmental

regulation, economic slowdown and surplus

capacity, competition from other providers of

services and other factors.

Specific sector investing such as real estate

can be subject to different and greater risks

than more diversified investments. Declines in

the value of real estate, economic conditions,

property taxes, tax laws and interest rates

all present potential risks to real estate

investments.

Income from funds managed for tax efficiency

may be subject to an alternative minimum tax,

and/or any applicable state and local taxes.

Bond investors should carefully consider

risks such as interest rate, credit, default and

duration risks. Greater risk, such as increased

volatility, limited liquidity, prepayment,

non-payment and increased default risk, is

inherent in portfolios that invest in high-yield

(“junk”) bonds or mortgage-backed securities,

especially mortgage-backed securities with

exposure to subprime mortgages. Generally,

when interest rates rise, prices of fixed-income

securities fall.

Nothing contained in this material is

intended to constitute legal, tax, securities or

investment advice, nor an opinion regarding

the appropriateness of any investment.

The general information contained in this

publication should not be acted upon without

obtaining specific legal, tax and investment

advice from a licensed professional.

INDEX DEFINITIONS:

Russell 3000® Index: Index measures

the performance of the largest 3000 U.S.

companies representing approximately 98%

of the investable U.S. equity market. The

trademarks, service marks and copyrights

related to the Russell indexes and other

materials as noted are the property of their

respective owners.

S&P 500® Index: A free-float capitalizationweighted

index published since 1957 of the

prices of 500 large-cap common stocks

actively traded in the United States. The stocks

included in the S&P 500 are those of large

publicly held companies that trade on either

of the two largest American stock market

exchanges: the New York Stock Exchange and

the NASDAQ.

ABOUT MORNINGSTAR CATEGORY:

U.S. Equity Funds are mutual funds or

exchange-traded funds (ETFs) that invest at

least 75% of their total assets in equities, and

at least 75% of equity assets in US equities.

These funds invest primarily in the equities of

US companies across various capitalizations

and styles.

The Morningstar categories are as reported

by Morningstar and have not been modified.

© 2023 Morningstar, Inc. All Rights Reserved.

The information contained herein: (1) is

proprietary to Morningstar; (2) may not be

copied or distributed; and (3) is not warranted

to be accurate, complete or timely. Neither

Morningstar nor its content providers are

responsible for any damages or losses arising

from any use of this information.

GENERAL DISCLOSURES:

Russell Investments’ ownership is composed

of a majority stake held by funds managed

by TA Associates Management, L.P., with

a significant minority stake held by funds

managed by Reverence Capital Partners, L.P.

Certain of Russell Investments’ employees

and Hamilton Lane Advisors, LLC also hold

minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the

Russell trademarks contained in this material

and all trademark rights related to the Russell

trademarks, which the members of the

Russell Investments group of companies are

permitted to use under license from Frank

Russell Company. The members of the Russell

Investments group of companies are not

affiliated in any manner with Frank Russell

Company or any entity operating under the

“FTSE RUSSELL” brand.

Russell Investment Company mutual funds

are distributed by Russell Investments

Financial Services, LLC, member FINRA,

part of Russell Investments.

Copyright © 2024 Russell Investments

Group, LLC. All rights reserved. This material

is proprietary and may not be reproduced,

transferred, or distributed in any form

without prior written permission from Russell

Investment Group. It is delivered on an “as is”

basis without warranty.

First used: September 2024

RIFIS-26193_S (Exp. 08/26)